KMB leads the development of Korea's derivatives market by expendingits service areas through a strong network with domestic and foreign financial institutions.

Introduction

The local derivatives market was initially dominated by foreign brokers located abroad such as Hong Kong or Singapore.In 1996 KMB became the first domestic broker to launch derivatives broking services, and has since spearheaded the development of the nation's

derivatives market with diversified products including IRS, CRS and FRA.

Building on a very tight network with institutional customers home and abroad, we continue to make investment to hireand nurture extremely competent brokers equipped with strong expertise and adopt latest broking system.

Our commitment to the best broking services will remain unchanged in

order to provide precise index rates and maximize efficiency in the market.

Products

IRS

CRS

FRA

IRS

Interest Rate Swap (IRS) is a contract where two parties agree to exchange interest cash flows on a notional principal of thesame currency during the term of the agreement. Being used to hedge changes in interest rates, IRS has some variations such as"coupon swap" - exchanging a fixed rate for a floating rate (or vice versa) - and "basis swap" - exchanging a floating rate foranother with different tenors.

Clearing

KRW Deliberable IRS (Compulsory liquidation via KRX until plain vanilla swap of 20 years in unit of 3 months)

KRW Non-Deliverable IRS (In voluntary liquidation through LCH, CME, etc.)

USD IRS (In voluntary liquidation through KRX)

Section

Description

Note

Currency

KRW

Maturity

1, 2, 3, 4, 5, 7, 10, 12, 15, 20, 25 and 30 years & odd tenor

Unit

KRW 10 billion

KRW 10 billion in minimum transaction size

Trading Hour

No restriction

Price Quoting

Fixed rate (KRW) expressed in percentage

To 4 decimal places

Payment Frequency

3 months in principle, but 6 and 12 months, etc. also negotiable

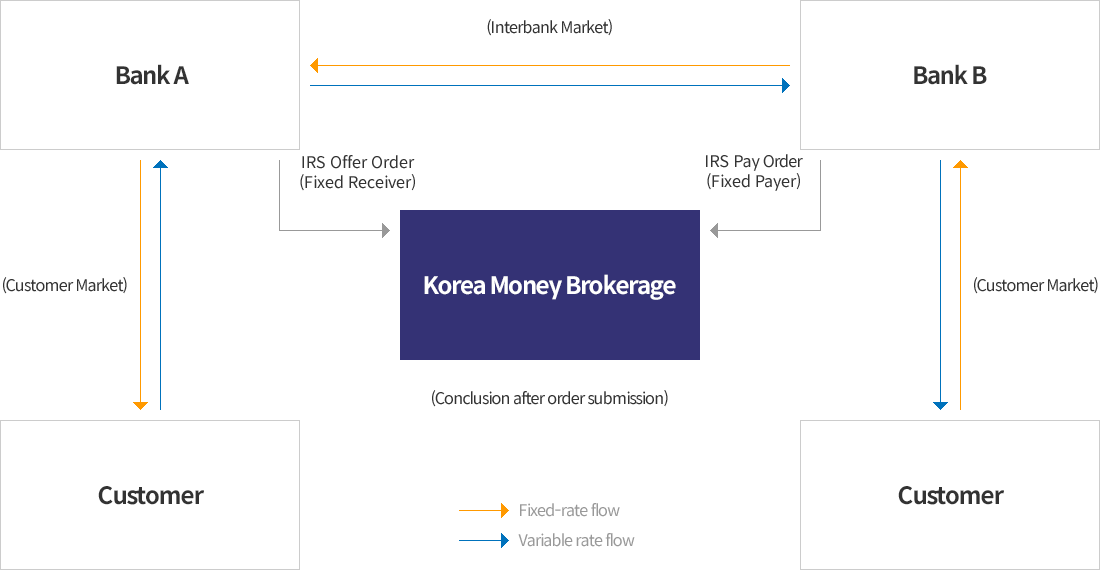

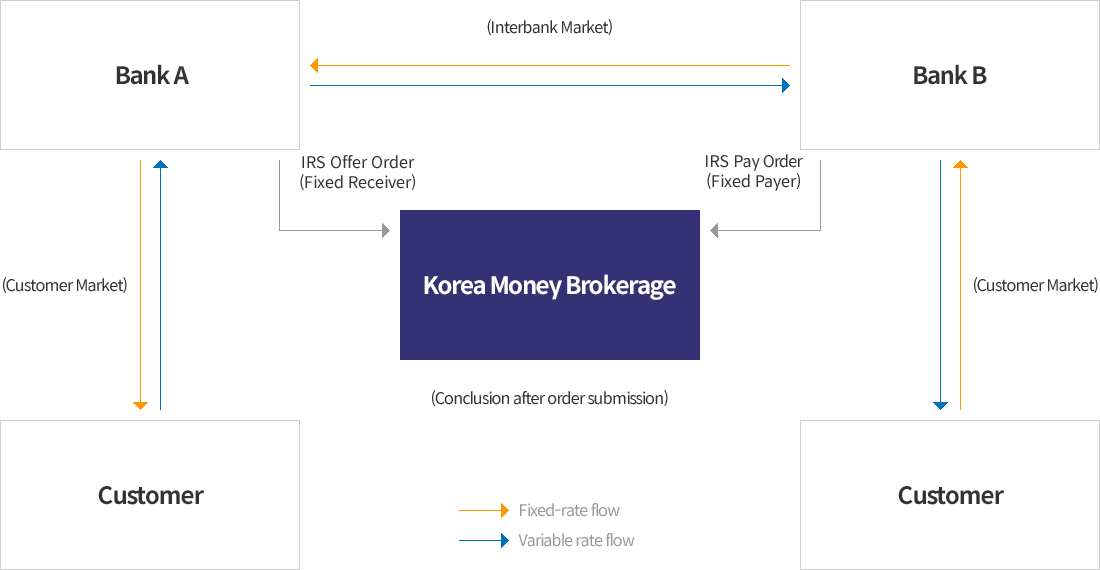

Transaction Flow

Transaction Flow Chart

CRS

Currency Swap (CRS) is an agreement involving the exchange of principal amounts in one currency for another at the beginningand end of the contract. The two parties exchange interest payment during the life of a swap and re-exchange the principal amountat maturity based on the rate at which the principal was exchanged at the beginning of the contract. The main use of CRS is toprovide a mid- and long-term hedge against currency risk and interest rate changes.

FRA is a derivative instrument designed to hedge future interest rate movement or take speculative profits.Two parties of the agreement exchange fixed and floating interest payment on a certain principalamount during a specified future period of time.

Section

Description

Note

Currency

KRW

Maturity

3 months from a certain point of time in the future1*4, 2*5, 3*6, 4*7, 5*8, 6*9, 9*12 months & odd tenor